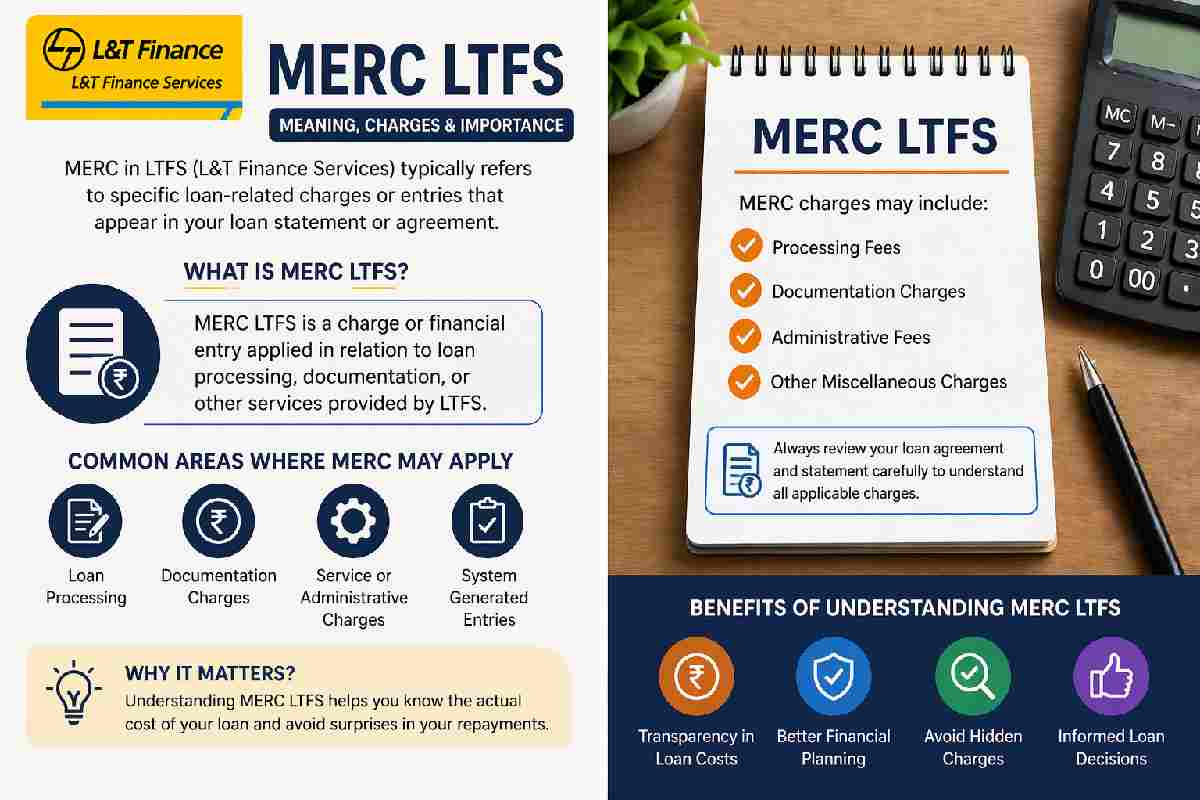

What is MERC LTFS? (Simple Explanation First)

If you’ve come across the term MERC LTFS, chances are you saw it in a loan document, EMI statement, or transaction detail related to L&T Finance Services (LTFS).

Here’s the simple explanation:

MERC LTFS usually refers to a charge, code, or internal financial entry used in LTFS loan processing or billing.

It’s not a widely defined public term like “interest rate” or “processing fee.” Instead, it often shows up as part of backend calculations or financial records.

That’s why many users get confused when they see it.

Key Takeaways

- MERC LTFS is linked to loan-related charges or entries

- It is not a standard public financial term

- Always check complete loan cost

- NBFC loans are fast but may be expensive

- Awareness helps avoid hidden charges

The Real Talk (What It Actually Means for You)

Let’s be honest.

When most people search for MERC LTFS, they’re not looking for a technical definition. They’re worried about one thing:

“Am I being charged something extra?”

And that’s a valid concern.

In many cases, terms like MERC are linked to:

- Additional service charges

- System-generated financial entries

- Loan-related adjustments

So instead of focusing only on the name, what really matters is:

Does it increase your total repayment?

If yes — you need to understand it properly.

About L&T Finance Services (LTFS)

L&T Finance is a major Non-Banking Financial Company (NBFC) in India. It provides loans to millions of customers across the country.

Some common services include:

- Personal loans

- Two-wheeler loans

- Business loans

- Rural and microfinance

Because NBFCs are designed for faster approvals, they often:

- Process loans quickly

- Require fewer documents

- But may charge slightly higher interest or fees

Where You Might See MERC LTFS

You might notice this term in:

- Loan statements

- EMI breakdowns

- Bank transaction descriptions

- Digital loan apps

It’s usually not highlighted or explained clearly — which is why it creates confusion.

Types of Charges in LTFS Loans

To understand MERC better, you need to know the types of charges typically included in loans.

1. Processing Fee

Charged when your loan is approved.

2. Interest Rate

The main cost of borrowing.

3. Late Payment Charges

Applied if you miss an EMI.

4. Prepayment Charges

If you repay early.

5. Miscellaneous Charges (Where MERC fits in)

This is where entries like MERC usually fall.

These are often small but add up over time.

Who Should Pay Attention to This?

You should care about MERC LTFS if:

- You have taken a loan from LTFS

- You see unexplained charges

- Your EMI total seems higher than expected

You should be extra careful if:

- You’re a first-time borrower

- You didn’t read full terms

- You chose a long loan tenure

Interest Rates in India (Realistic Range)

Interest rates vary depending on your profile, but here’s a realistic idea:

| Loan Type |

Interest Rate |

| Personal Loan |

11% – 24% |

| Bike Loan |

9% – 18% |

| Business Loan |

12% – 22% |

NBFCs like LTFS usually fall on the higher side compared to banks.

Benefits of Taking Loan from LTFS

Fast Approval

You can get loans quickly, sometimes within hours.

Less Documentation

Ideal for self-employed users.

Easy Access

Available even in smaller towns.

Drawbacks You Should Not Ignore

Higher Cost

Interest + extra charges = higher total repayment.

Hidden Fees

Terms like MERC may confuse users.

Penalties

Late payments can become expensive.

Common Mistakes People Make

Here’s what most borrowers get wrong:

- Looking only at EMI, not total cost

- Ignoring small charges

- Not asking questions

- Taking loans without comparison

These mistakes lead to paying more than expected.

Real-Life Scenario (Simple Example)

Let’s say:

- Loan Amount: ₹1,00,000

- Interest: 18%

- Tenure: 3 years

Your EMI may look manageable.

But when you add:

- Processing fee

- GST

- Extra charges (like MERC-type entries)

Your total repayment can increase significantly.

How to Stay Safe (Practical Tips)

If you want to avoid surprises:

Always read the loan agreement

Even small terms matter.

Ask customer support

If you see unknown entries like MERC.

Use EMI calculators

Check total payable amount.

Compare lenders

Don’t take the first loan you see.

Myths vs Reality

| Myth |

Reality |

| NBFC loans are always cheap |

Often more expensive than banks |

| EMI is the only cost |

Total repayment matters more |

| Small charges don’t matter |

They add up over time |

Who Should Take LTFS Loans?

Good for:

- Urgent financial needs

- People with limited credit history

- Small business owners

Not ideal for:

- Long-term borrowing

- People looking for lowest interest

- Those who don’t read terms carefully

Final Thoughts

The term MERC LTFS may look confusing, but it’s not something mysterious or dangerous by itself. It’s simply part of the financial system used in loan processing.

What matters is how aware you are as a borrower. If you understand your loan completely, no hidden term can surprise you.

Always remember:

- Focus on total cost, not just EMI

- Ask questions when confused

- Read everything before signing

That’s how you stay in control of your money.

Conclusion

Understanding terms like MERC LTFS is less about decoding the name and more about being financially aware. Whether you are taking a personal loan or financing a purchase, clarity is your biggest advantage.

Take your time, read carefully, and never hesitate to ask questions. That’s the difference between a smart borrower and a stressed one.

FAQs

1. What does MERC LTFS mean?

It usually refers to a financial entry or charge related to LTFS loan processing.

2. Is MERC a hidden charge?

Not always hidden, but it may not be clearly explained.

3. Is L&T Finance safe?

Yes, it is a regulated NBFC in India.

4. Why is my loan amount higher than expected?

Due to additional charges beyond EMI, including fees and taxes.

5. Can I avoid extra charges?

Yes, by reading terms carefully and paying on time.

Wikipedia Reference

https://en.wikipedia.org/wiki/L%26T_Finance

{kind=link}